Printable California Loan Agreement Form

Printable California Loan Agreement Form

Incomplete Information: Many individuals fail to provide all necessary details. This includes missing personal information such as full names, addresses, and contact numbers. Omitting any part of this information can lead to delays or complications in the loan process.

Incorrect Loan Amount: Some borrowers mistakenly enter an incorrect loan amount. This can happen due to simple math errors or misunderstandings about the total needed. Ensuring that the requested amount matches the intended purpose is crucial.

Neglecting Signatures: A common oversight is forgetting to sign the document. Without signatures from all parties involved, the agreement is not legally binding. It’s essential to double-check that every required signature is present before submission.

Not Reviewing Terms: Failing to read and understand the loan terms can lead to misunderstandings later on. Borrowers should carefully review interest rates, repayment schedules, and any fees associated with the loan. Clarity on these points is vital to avoid future disputes.

Filling out a California Loan Agreement form can seem daunting, but understanding its key components makes the process smoother. Here are nine essential takeaways to keep in mind:

By following these key points, you can confidently navigate the process of completing a California Loan Agreement form.

What is a California Loan Agreement?

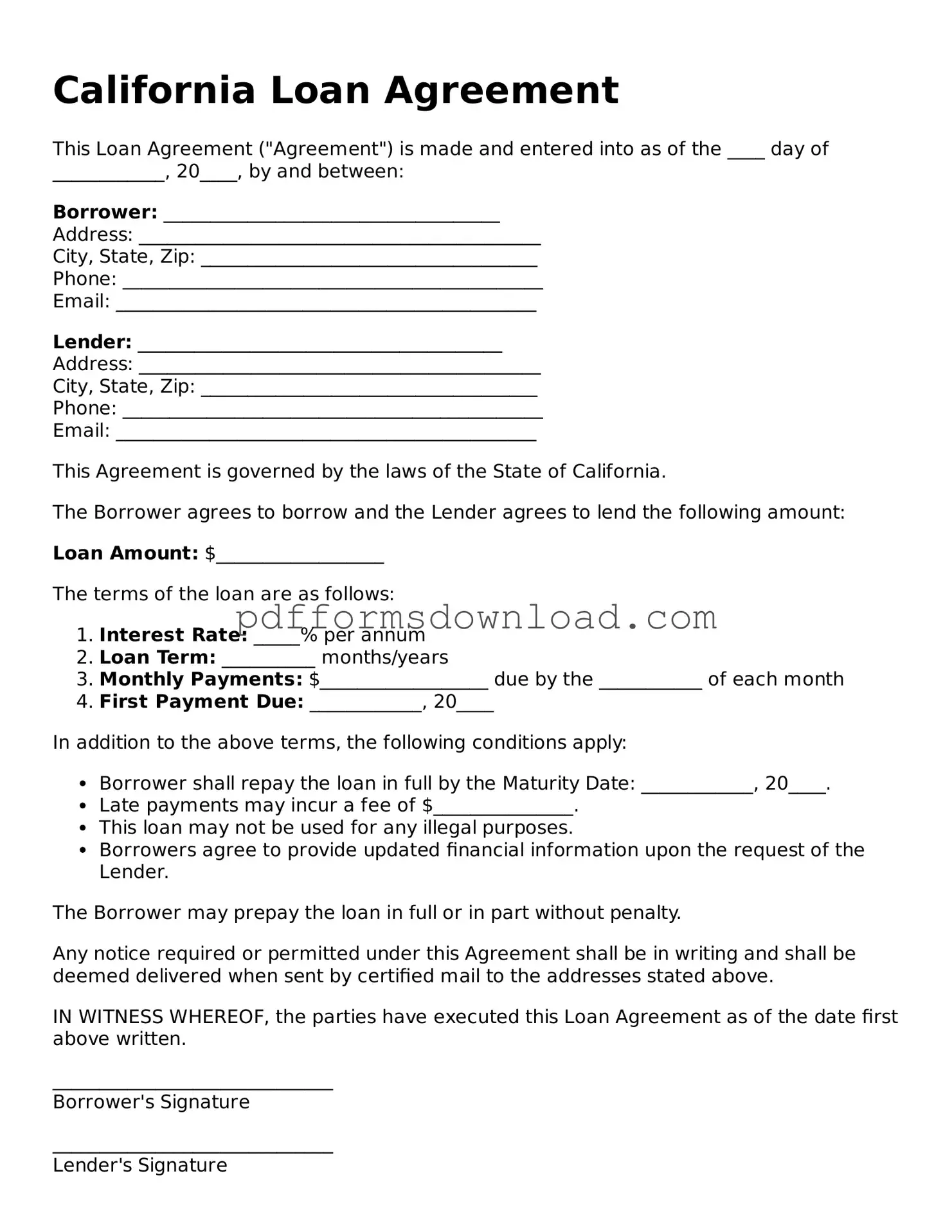

A California Loan Agreement is a legal document outlining the terms and conditions of a loan between a lender and a borrower. It specifies details such as the loan amount, interest rate, repayment schedule, and any collateral involved. This document helps protect the rights of both parties and ensures clarity in the loan process.

Who can use a California Loan Agreement?

Any individual or business in California can use a Loan Agreement. This includes personal loans between friends or family members, as well as formal loans between businesses or financial institutions. It is important that both parties understand the terms before signing.

What are the key components of a California Loan Agreement?

Key components typically include the loan amount, interest rate, repayment terms, due dates, and any fees associated with the loan. Additionally, the agreement may outline the consequences of defaulting on the loan and any collateral that secures the loan.

Is a California Loan Agreement legally binding?

Yes, once both parties sign the Loan Agreement, it becomes a legally binding contract. This means that both the lender and borrower are obligated to adhere to the terms outlined in the document. If either party fails to comply, legal action may be pursued.

Do I need a lawyer to create a California Loan Agreement?

While it is not legally required to have a lawyer draft a Loan Agreement, it is advisable to seek legal counsel if you have questions or concerns. A lawyer can help ensure that the agreement complies with California laws and meets the specific needs of both parties.

Can I modify a California Loan Agreement after it is signed?

Yes, a Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It is recommended to document any modifications in writing and have both parties sign the amended agreement to avoid future disputes.

What happens if I default on a loan outlined in the California Loan Agreement?

If a borrower defaults on the loan, the lender may take legal action to recover the owed amount. This could include pursuing collections or initiating a lawsuit. The specific consequences of defaulting should be clearly stated in the Loan Agreement.

How can I ensure my California Loan Agreement is enforceable?

To ensure enforceability, both parties should fully understand the terms before signing. The agreement should be clear, concise, and free of ambiguous language. Additionally, it is important to keep a signed copy of the agreement for your records.

When entering into a loan agreement in California, several additional forms and documents often accompany the primary loan agreement. Each of these documents serves a specific purpose, ensuring that both the lender and borrower are protected and informed throughout the lending process. Understanding these documents can help facilitate a smoother transaction.

Understanding these documents can empower borrowers and lenders alike, fostering a clearer understanding of their rights and responsibilities. When armed with the right information, all parties can navigate the lending process with confidence and clarity.

New York Promissory Note - The Loan Agreement should be signed by both parties.

To ensure a smooth transaction in the sale of a mobile home, it is essential to have the proper documentation. This includes the New York Mobile Home Bill of Sale form, which clearly details the necessary information about the buyer, seller, and the mobile home. For convenience, you can download and fill out the form to formalize your agreement and protect your interests during the sale process.

Texas Promissory Note Requirements - Loan Agreements may require periodic updates to account for changing regulations.