Download Cg 20 10 07 04 Liability Endorsement Template

Download Cg 20 10 07 04 Liability Endorsement Template

Neglecting to fill in the policy number: One of the most common mistakes is failing to enter the correct policy number at the top of the form. This can lead to confusion and delays in processing the endorsement.

Incorrectly listing additional insureds: People often make the mistake of misspelling the names of the additional insured persons or organizations. Accuracy is crucial, as even a small error can render the endorsement invalid.

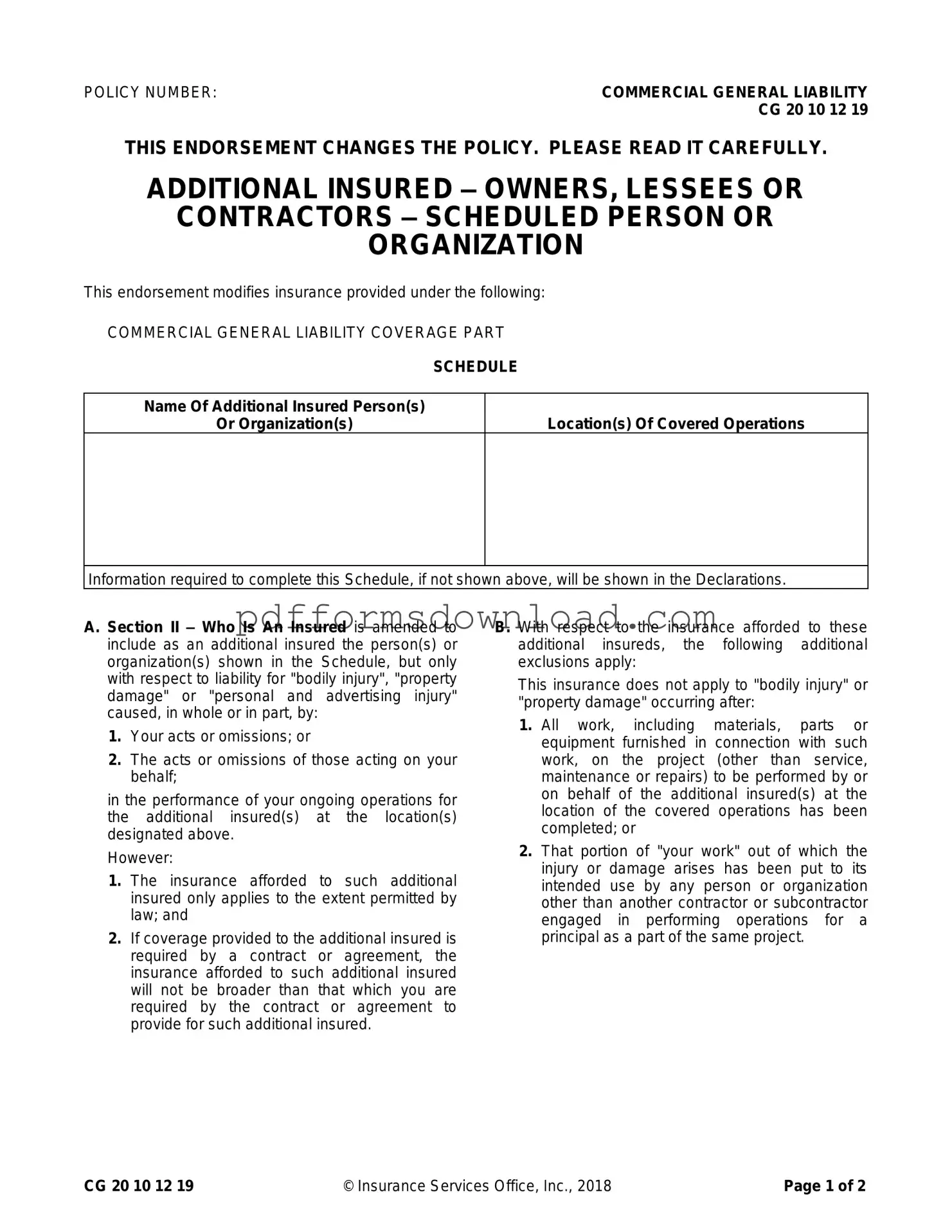

Omitting the location of covered operations: Leaving out the specific locations where the coverage applies can create gaps in protection. It is essential to clearly state where the operations will take place.

Failing to understand the limitations of coverage: Many individuals do not fully grasp the limitations and exclusions outlined in the endorsement. This can lead to unrealistic expectations regarding what is covered.

Not reviewing contractual obligations: Some people forget to check their contracts for specific insurance requirements. The coverage provided cannot exceed what is required by any existing agreements.

Ignoring the completion of work clause: It’s important to pay attention to the clause regarding when coverage ends, specifically after all work on the project is completed. Ignoring this can result in unexpected liability issues.

Submitting the form without a thorough review: Rushing to submit the form without a final review can lead to overlooked mistakes. Taking a moment to double-check all entries can save time and prevent complications later.

When using the CG 20 10 07 04 Liability Endorsement form, it's important to understand its key features and requirements. Here are some essential takeaways:

Understanding these key points will help ensure that you fill out and utilize the form correctly, providing the necessary coverage for all parties involved.

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form serves to add specific individuals or organizations as additional insureds under a Commercial General Liability policy. This is particularly important for contractors, as it helps protect them from liability claims that may arise during their operations for the additional insureds. By including this endorsement, the policy ensures that both the contractor and the additional insureds have coverage for certain liabilities related to bodily injury, property damage, or personal and advertising injury.

Who qualifies as an additional insured under this endorsement?

Individuals or organizations listed in the endorsement's schedule qualify as additional insureds. They are covered only for liabilities resulting from the contractor's actions or omissions while performing work for them. It's crucial to note that this coverage is limited to the locations and operations specified in the endorsement, ensuring that it is relevant to the specific project or contract.

What limitations exist regarding the coverage for additional insureds?

Coverage for additional insureds is subject to certain limitations. For instance, the endorsement does not apply to bodily injury or property damage occurring after the contractor has completed all work on the project, except for ongoing maintenance or repairs. Additionally, if the work has been put to its intended use by someone other than a contractor involved in the same project, the coverage may not apply. This means that the timing and context of the work are critical factors in determining coverage.

How does this endorsement affect the limits of insurance?

The endorsement specifies that it does not increase the overall limits of insurance provided by the policy. If coverage for an additional insured is required by a contract, the maximum amount payable will be the lesser of the limit specified in the contract or the applicable limits of the insurance policy. This ensures that the coverage remains within the bounds of the original policy limits while fulfilling contractual obligations.

Are there any additional exclusions for additional insureds?

Yes, the endorsement includes specific exclusions for additional insureds. For example, it does not cover bodily injury or property damage that occurs after the completion of the contractor's work. This means that any claims arising after the project has been finished may not be covered under this endorsement, emphasizing the importance of timing in liability claims.

What should be included in the schedule section of the endorsement?

The schedule section should list the names of the additional insured persons or organizations, as well as the locations of the covered operations. This information is crucial for determining who is covered and under what circumstances. If any required information is not provided in the schedule, it will be included in the policy's declarations, ensuring clarity and compliance with the endorsement's terms.

Can the coverage for additional insureds be broader than what is required by contract?

No, the coverage afforded to additional insureds cannot be broader than what is stipulated in the contract or agreement. This means that if a contract specifies certain limits or types of coverage, the endorsement will align with those requirements. This provision helps maintain consistency between contractual obligations and insurance coverage, preventing any misunderstandings about the extent of protection provided.

When dealing with insurance and liability coverage, several forms and documents complement the CG 20 10 07 04 Liability Endorsement form. Each of these documents plays a critical role in ensuring clarity and protection for all parties involved in a contractual agreement. Understanding these documents can help you navigate the complexities of liability insurance effectively.

Each of these documents contributes to a comprehensive understanding of liability coverage and risk management in business operations. Familiarity with them not only aids in compliance but also fosters stronger partnerships and mitigates potential disputes.

What Do Immunization Records Look Like - The Immunization Record form provides essential information about your child's vaccinations.

Free Printable Act of Donation Form Louisiana - The donor must consider any tax implications associated with the act of donation.

To effectively launch a business in California, understanding the essential steps is vital, including the completion of the California Articles of Incorporation form, which serves to legally establish your corporation. This form, found at https://californiadocsonline.com/articles-of-incorporation-form, requires you to provide key details such as the corporation’s name, purpose, and structure, making it a crucial part of your entrepreneurial journey.

Girlfriend Application - Desires a connection that is both deep and meaningful.