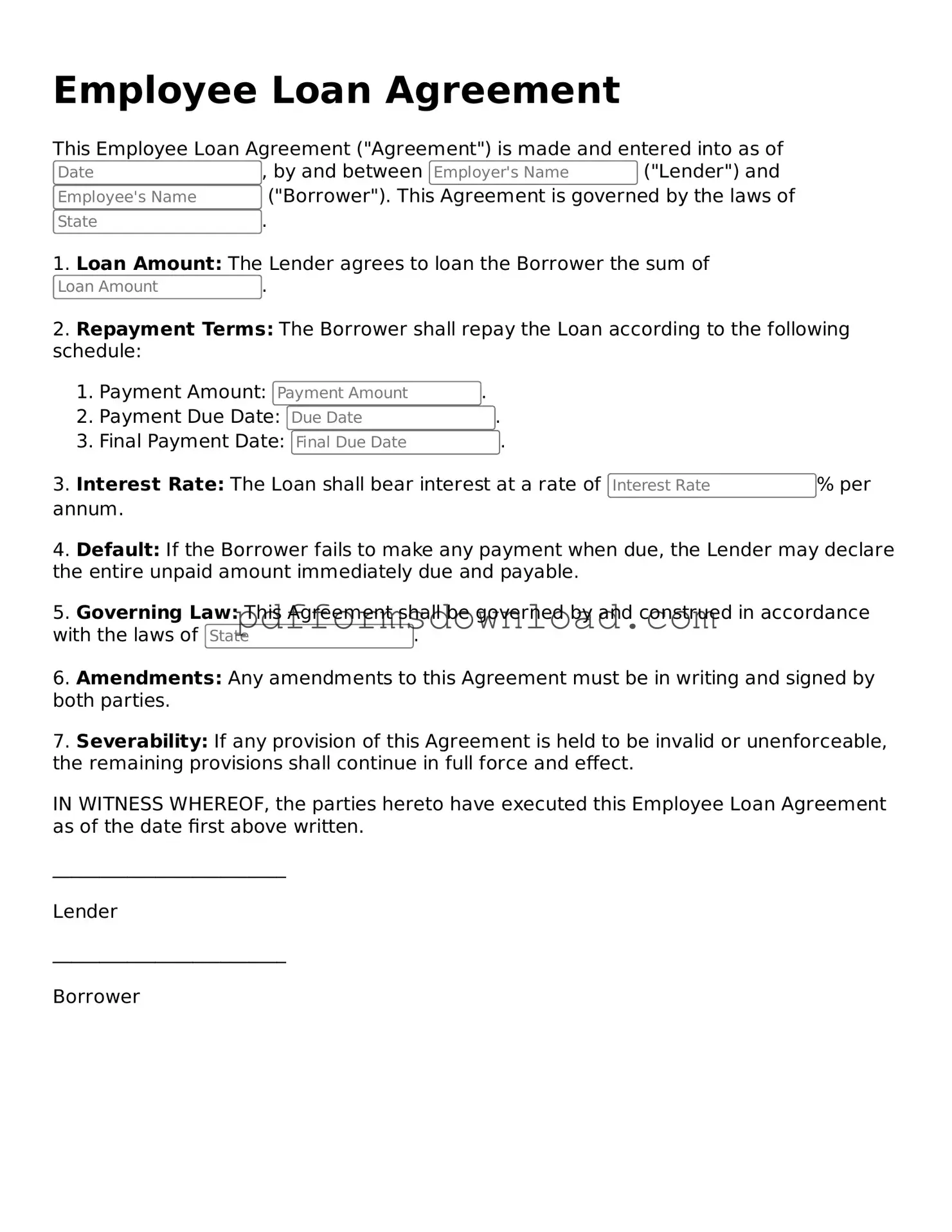

Official Employee Loan Agreement Document

Official Employee Loan Agreement Document

Not reading the agreement thoroughly: Many individuals skim through the document without understanding the terms. This can lead to misunderstandings about repayment schedules and interest rates.

Failing to provide accurate personal information: Inaccurate details such as name, address, or Social Security number can create complications in processing the loan.

Overlooking the loan amount: Some may request a loan amount that exceeds what they are eligible for, leading to delays or rejections.

Ignoring repayment terms: It's crucial to understand the repayment schedule. Missing a payment can have serious consequences.

Not considering the interest rate: Some borrowers fail to calculate how much interest will accumulate over time, which can affect their financial planning.

Neglecting to ask questions: If something is unclear, it’s important to seek clarification. Ignorance can lead to costly mistakes.

Forgetting to sign and date the form: A common oversight is failing to sign the agreement, which can render it invalid.

Not keeping a copy: After submitting the form, it’s wise to retain a copy for personal records. This can help in future reference and accountability.

Assuming all loans are the same: Each loan agreement can have unique terms. Treating them all as identical can lead to unexpected challenges.

Disregarding the consequences of default: Failing to understand what happens if payments are missed can lead to dire financial repercussions.

When utilizing the Employee Loan Agreement form, it is crucial to understand its significance and the responsibilities it entails. Here are some key takeaways to consider:

By keeping these points in mind, both employers and employees can navigate the loan process with greater confidence and understanding.

What is an Employee Loan Agreement?

An Employee Loan Agreement is a formal document that outlines the terms and conditions under which an employer provides a loan to an employee. This agreement details the loan amount, repayment schedule, interest rates (if applicable), and any other relevant terms. It serves to protect both the employer and the employee by clearly defining expectations and responsibilities.

Who can apply for an Employee Loan?

Typically, any employee who meets the eligibility criteria set by the employer can apply for an Employee Loan. These criteria may include factors such as length of employment, job performance, and financial need. It’s important to check with your HR department or the specific policies of your organization to understand who qualifies.

What information is included in the Employee Loan Agreement?

The Employee Loan Agreement usually includes several key pieces of information. This includes the total loan amount, the interest rate (if any), the repayment schedule, and the duration of the loan. Additionally, it may outline any fees associated with late payments and the consequences of defaulting on the loan. Clear terms help both parties understand their obligations.

How is the repayment of the loan structured?

Repayment of the loan is often structured in regular installments, which can be deducted directly from the employee's paycheck. The agreement will specify the frequency of these payments—weekly, bi-weekly, or monthly—and the total duration of the repayment period. This ensures that the employee can budget effectively while fulfilling their repayment obligations.

What happens if an employee leaves the company before the loan is fully repaid?

If an employee leaves the company before repaying the loan, the agreement typically stipulates how the remaining balance must be handled. In many cases, the full amount may become due immediately. Some employers may allow for continued repayment through other means, such as direct payments. It's crucial to review the agreement to understand the specific terms related to this situation.

Can the terms of the Employee Loan Agreement be modified?

Yes, the terms of the Employee Loan Agreement can often be modified, but this usually requires mutual consent from both the employer and the employee. If circumstances change—such as financial hardship or changes in employment status—either party may request a review and potential modification of the terms. It’s advisable to document any changes in writing to ensure clarity and avoid misunderstandings.

When an Employee Loan Agreement is in place, several other documents often accompany it to ensure clarity and compliance. These documents help protect both the employer and the employee by outlining terms, responsibilities, and repayment processes. Below are some commonly used forms and documents related to employee loans.

Having these documents in place alongside the Employee Loan Agreement can help ensure a smooth process for both the employer and the employee. Clear communication and well-documented agreements are key to avoiding misunderstandings.