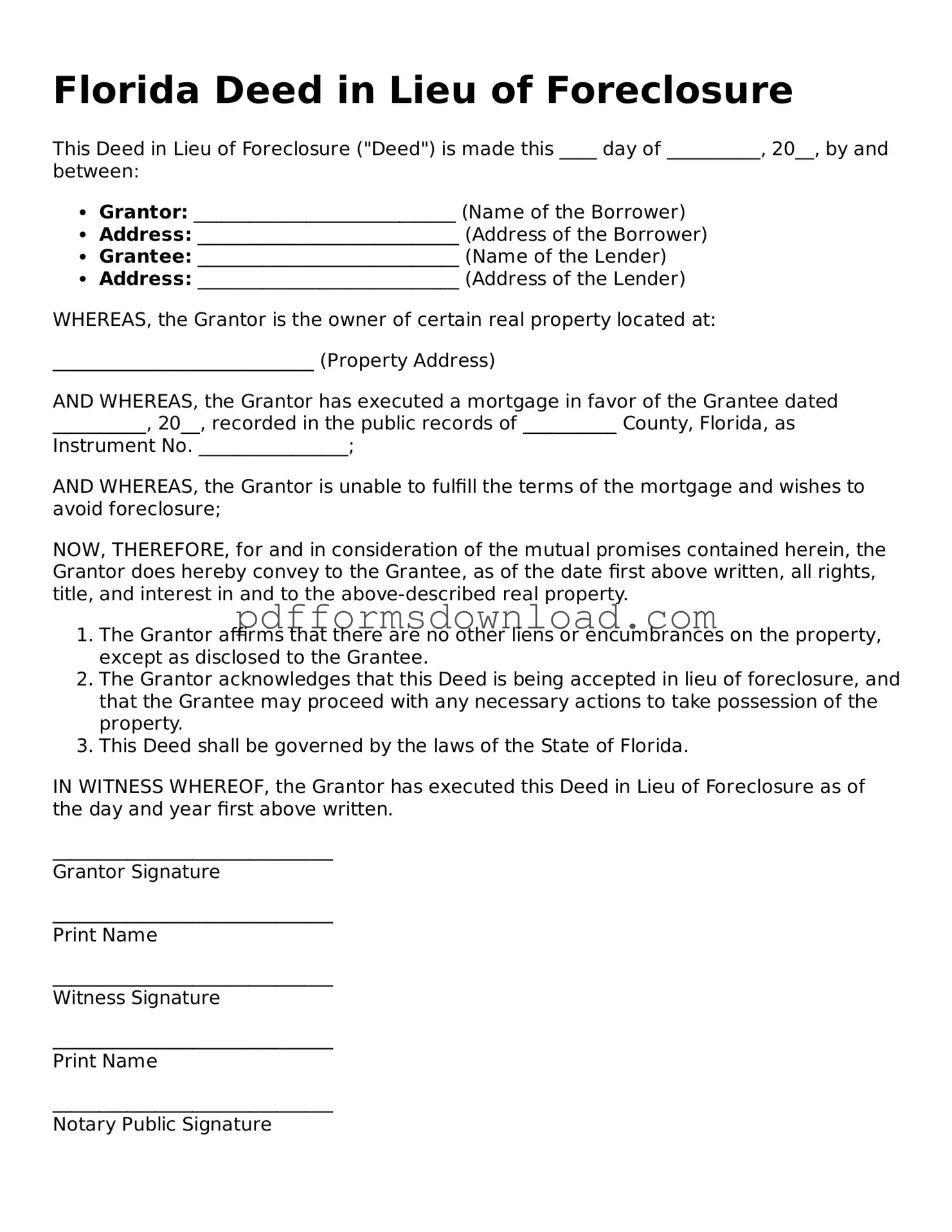

Printable Florida Deed in Lieu of Foreclosure Form

Printable Florida Deed in Lieu of Foreclosure Form

Not Including All Required Information: Many people forget to fill in all necessary details. This includes the names of all parties involved, property address, and legal descriptions. Missing even one piece of information can delay the process.

Failing to Sign and Date the Document: A common mistake is neglecting to sign or date the deed. Without a signature, the document is not valid. Make sure all parties sign and date the form to avoid complications.

Not Understanding the Consequences: Some individuals do not fully grasp the implications of a deed in lieu of foreclosure. This can affect credit scores and future homeownership opportunities. It’s crucial to understand what you are agreeing to before signing.

Ignoring Local Laws and Regulations: Each state has specific laws regarding deeds in lieu of foreclosure. Ignoring these can lead to legal issues. Always check Florida’s regulations to ensure compliance with local requirements.

When considering a Deed in Lieu of Foreclosure in Florida, it is essential to understand the implications and requirements of the process. Here are key takeaways to keep in mind:

By following these steps, homeowners can better navigate the Deed in Lieu of Foreclosure process in Florida.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer ownership of their property back to the lender to avoid the foreclosure process. This option is often considered when a homeowner can no longer afford their mortgage payments and wants to minimize the impact on their credit score. By voluntarily giving up the property, the homeowner may be able to avoid the lengthy and costly foreclosure proceedings.

What are the benefits of choosing a Deed in Lieu of Foreclosure?

There are several advantages to opting for a Deed in Lieu of Foreclosure. First, it can help homeowners avoid the negative consequences of a foreclosure on their credit report. Typically, a Deed in Lieu may have a less severe impact on credit scores compared to a foreclosure. Additionally, the process is generally quicker and less expensive than going through foreclosure. Homeowners may also have the opportunity to negotiate with the lender for a potential waiver of any deficiency balance, meaning they won’t owe any remaining debt after the property is transferred.

What are the requirements to qualify for a Deed in Lieu of Foreclosure?

To qualify for a Deed in Lieu of Foreclosure, homeowners must typically demonstrate financial hardship and provide documentation of their inability to continue making mortgage payments. Lenders often require a complete financial disclosure, including income, expenses, and any other debts. Homeowners should also be current on their mortgage payments or at least not more than one or two payments behind. Each lender may have its own specific criteria, so it's essential to communicate directly with the lender to understand their requirements.

How does the process of executing a Deed in Lieu of Foreclosure work?

The process begins with the homeowner contacting their lender to express interest in a Deed in Lieu of Foreclosure. After the lender reviews the homeowner's financial situation, they may approve the request. Once approved, both parties will need to sign the Deed in Lieu document, which officially transfers ownership of the property to the lender. After the signing, the lender will typically record the deed with the county clerk’s office. It’s important for homeowners to seek legal advice throughout this process to ensure they understand their rights and obligations.

A Deed in Lieu of Foreclosure can be a strategic option for homeowners facing financial difficulties. It allows the homeowner to transfer ownership of the property back to the lender, thereby avoiding a lengthy foreclosure process. However, several other forms and documents are often used in conjunction with this deed to ensure a smooth transition. Below is a list of these documents, each with a brief description.

Each of these documents plays a crucial role in the process surrounding a Deed in Lieu of Foreclosure. Understanding their purpose can help homeowners navigate this complex situation more effectively.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - The Deed in Lieu of Foreclosure can help borrowers avoid the extensive consequences of foreclosure on their credit report.

For those looking to navigate the legal requirements of vehicle transactions, a thorough understanding of the RV Bill of Sale form is crucial. To ensure a smooth transfer of ownership, consider utilizing resources such as the comprehensive RV Bill of Sale document, which helps in documenting key details of the sale. This form not only protects both parties involved but also facilitates the registration process under the new owner's name.

Will I Owe Money After a Deed in Lieu of Foreclosure - This form can also be beneficial for lenders, as it allows them to recover their loss without additional costs of foreclosure.