Printable Florida Promissory Note Form

Printable Florida Promissory Note Form

Incorrect Borrower Information: Many individuals fail to provide accurate details about the borrower. This includes the full name, address, and contact information. Ensure that all information is current and correctly spelled.

Missing Lender Information: It's essential to include the lender's information as well. Omitting the lender's name and address can lead to confusion later on.

Ambiguous Loan Amount: Some people write the loan amount in words but forget to include the numerical figure, or vice versa. Both formats should be present to avoid any misunderstandings.

Undefined Interest Rate: Not specifying the interest rate can create disputes. Clearly state whether the loan is interest-free or include the percentage rate if applicable.

Vague Payment Terms: It’s crucial to outline the repayment schedule. Many forget to specify how often payments are due (monthly, quarterly, etc.) and the total duration of the loan.

Neglecting Signatures: Both the borrower and lender must sign the document. Forgetting to sign can invalidate the agreement, so be sure to check for signatures before finalizing.

Failing to Date the Document: A common oversight is not dating the promissory note. The date is important as it marks the start of the loan agreement and can affect the repayment timeline.

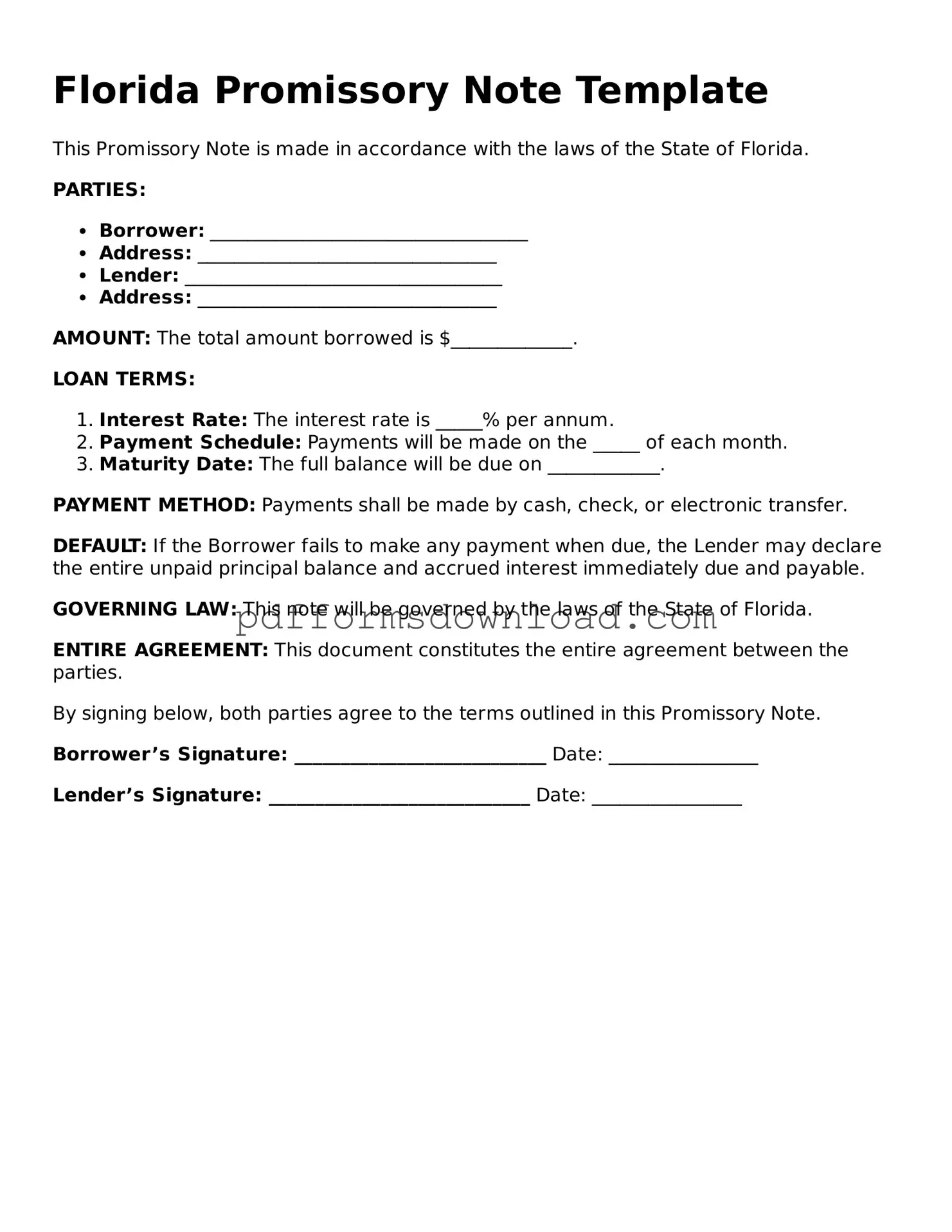

The Florida Promissory Note is a legally binding document that outlines the terms of a loan between a borrower and a lender.

It is essential to include the principal amount, interest rate, and repayment schedule clearly to avoid any misunderstandings.

Both parties should sign the note to validate the agreement. This step is crucial for enforceability.

Consider specifying the consequences of defaulting on the loan, such as late fees or acceleration of the debt.

Ensure that the note complies with Florida state laws, which may include specific requirements regarding interest rates and terms.

Keep a copy of the signed Promissory Note for your records. This document serves as proof of the agreement.

Consulting with a legal professional can help clarify any uncertainties and ensure the document meets your needs.

What is a Florida Promissory Note?

A Florida Promissory Note is a legal document that serves as a written promise from one party to pay a specific sum of money to another party under agreed-upon terms. This document outlines the loan amount, interest rate, repayment schedule, and other important conditions. It acts as a record of the debt and can be enforced in court if necessary.

Who can use a Promissory Note in Florida?

Any individual or business can use a Promissory Note in Florida. Whether you are lending money to a friend, family member, or a business, having a written note protects both parties. It clarifies the terms and helps avoid misunderstandings in the future.

What are the essential components of a Florida Promissory Note?

A well-drafted Promissory Note should include the following key components: the names of the borrower and lender, the loan amount, the interest rate (if applicable), the repayment schedule, and any collateral securing the loan. Additionally, it should specify what happens in case of default, including any penalties or fees.

Do I need a lawyer to create a Promissory Note in Florida?

While it is not legally required to hire a lawyer to create a Promissory Note, doing so can be beneficial. A legal professional can ensure that the document is properly drafted and complies with Florida laws. This can provide peace of mind and help avoid potential disputes down the line.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note. This helps maintain clarity and protects the interests of both the borrower and lender.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has several options. They can pursue legal action to recover the owed amount, potentially leading to a court judgment. The terms of the Promissory Note will dictate the lender's rights and remedies in the event of default, so it is crucial to understand these provisions beforehand.

Is a Promissory Note enforceable in Florida?

Yes, a properly executed Promissory Note is enforceable in Florida. If the borrower fails to repay the loan as agreed, the lender can take legal action to collect the debt. Having a signed note strengthens the lender's position in court, making it easier to recover the owed amount.

Are there any tax implications related to a Promissory Note?

Yes, there can be tax implications associated with a Promissory Note. For example, the lender may need to report interest income on their tax return, while the borrower may be able to deduct interest payments if the loan qualifies. It is advisable to consult a tax professional to understand the specific implications based on your situation.

When dealing with a Florida Promissory Note, several other forms and documents may be necessary to ensure clarity and legal protection for all parties involved. Below is a list of commonly used documents that often accompany a Promissory Note.

Having these documents prepared and organized can streamline the lending process and protect the interests of both borrowers and lenders. Always consider consulting a professional to ensure that all necessary paperwork is completed accurately.

Promissory Note Virginia - The document can also describe any prepayment penalties, if applicable.

Personal Loan Promissory Note - The note is particularly useful for informal loans between friends and family.

A Non-disclosure Agreement (NDA) in Ohio is a legal document designed to protect sensitive information shared between parties. It ensures that confidential information remains private, safeguarding business interests and personal data. For those seeking to understand the nuances and processes associated with these agreements, resources like Ohio PDF Forms can be invaluable in providing guidance and assistance.

California Promissory Note - This form establishes a borrower's obligation to repay a loan, including payment terms and interest details.