Download IRS 1120 Template

Download IRS 1120 Template

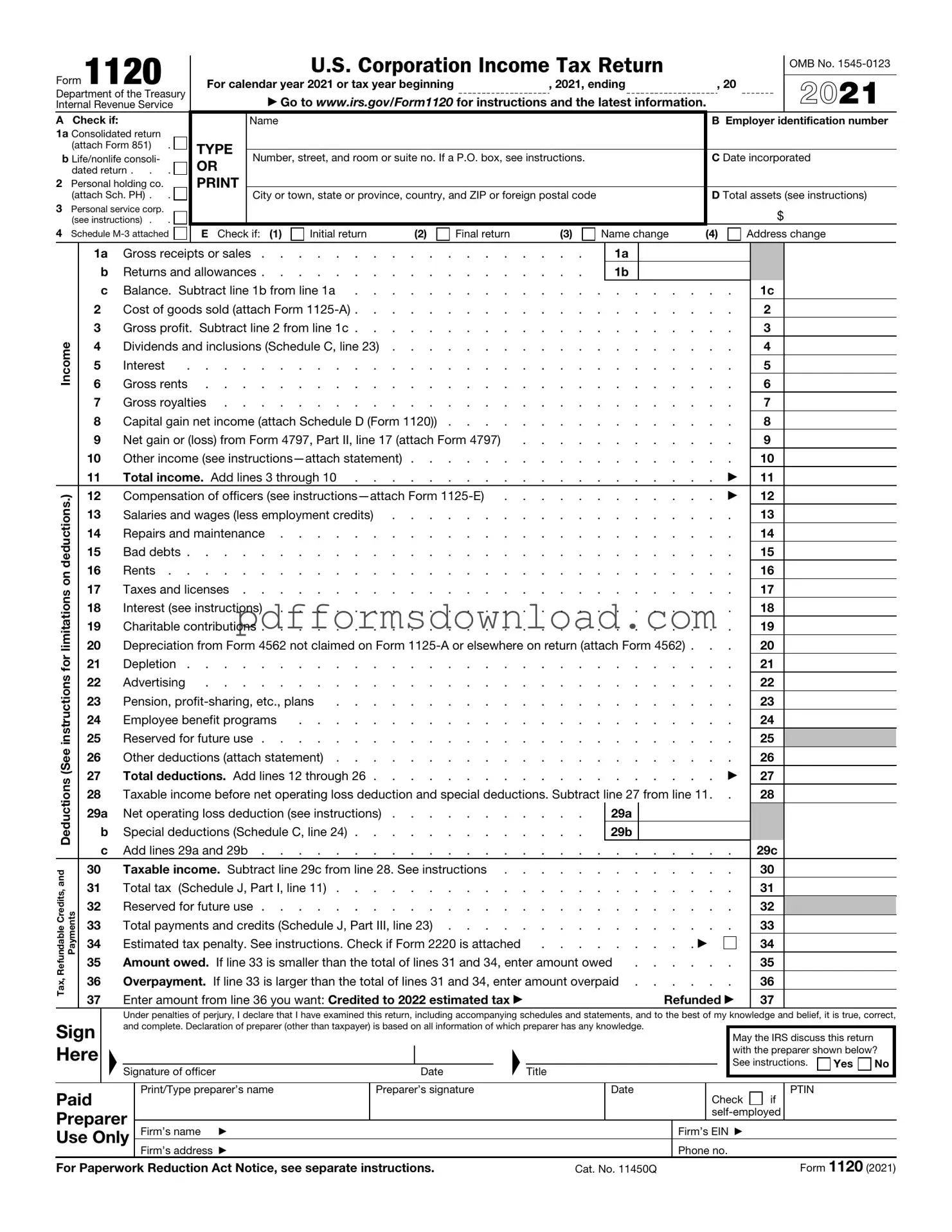

Incorrect Business Information: Many individuals fail to provide accurate details about their business. This includes the legal name, address, and Employer Identification Number (EIN). Errors in this section can lead to processing delays or issues with the IRS.

Misreporting Income: It's common for businesses to miscalculate their total income. This can occur due to overlooking certain revenue streams or failing to include all necessary documentation. Accurate reporting is crucial for compliance.

Neglecting Deductions: Some filers overlook potential deductions that could significantly lower their tax liability. Expenses such as salaries, rent, and utilities should be carefully reviewed and documented to ensure no eligible deductions are missed.

Inaccurate Tax Calculation: Mistakes in calculating the tax owed can lead to underpayment or overpayment. Double-checking the math and using the correct tax rates is essential to avoid complications.

Missing Signatures: A common oversight is forgetting to sign the form. Without a signature, the IRS may consider the submission invalid. It's important to ensure that all required signatures are present before sending the form.

Filing the IRS Form 1120 is an essential task for corporations operating in the United States. Understanding how to complete this form accurately can save time and resources. Here are some key takeaways to keep in mind:

By keeping these points in mind, corporations can navigate the complexities of the IRS Form 1120 with greater ease and confidence.

What is the IRS 1120 form used for?

The IRS 1120 form is primarily used by corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). This form helps the IRS assess the corporation's tax liability. Corporations must file this form annually, detailing their financial activities for the year. By doing so, they ensure compliance with federal tax laws and regulations, while also providing transparency regarding their financial performance.

Who is required to file Form 1120?

Any corporation that operates in the United States must file Form 1120, regardless of whether it is a domestic or foreign corporation doing business in the U.S. This includes C corporations, which are taxed separately from their owners. However, S corporations file a different form (Form 1120-S) to report income, as they pass their income directly to shareholders to avoid double taxation. It's important for corporations to determine their filing requirements based on their classification and activities.

When is the deadline for filing Form 1120?

The deadline for filing Form 1120 is typically the 15th day of the fourth month after the end of the corporation's tax year. For most corporations that operate on a calendar year, this means the form is due on April 15. If the deadline falls on a weekend or holiday, the due date is extended to the next business day. Corporations can also apply for an extension, which allows them to file up to six months later, but they must still pay any taxes owed by the original deadline to avoid penalties.

What are the penalties for not filing Form 1120 on time?

Failing to file Form 1120 on time can result in significant penalties. The IRS typically imposes a penalty based on the number of months the return is late, starting at $210 per month for each month the return is overdue, up to a maximum of 12 months. Additionally, if the corporation owes taxes and fails to pay them on time, interest will accrue on the unpaid amount. To avoid these penalties, it is crucial for corporations to file their returns accurately and on time.

The IRS Form 1120 is the U.S. Corporation Income Tax Return, which corporations use to report their income, gains, losses, deductions, and credits. Along with this form, several other documents are often required to provide a complete picture of a corporation's financial activities. Below are some common forms and documents that may accompany the IRS 1120.

These forms and documents play a crucial role in ensuring that corporations meet their tax obligations accurately. By providing detailed financial information, they help the IRS assess the corporation's tax liability effectively.

Direct Deposit Form Example - This form serves as an official document for payment transactions.

When navigating the responsibilities of purchasing an RV, it is crucial to understand the importance of an accurate document. This is where the thorough RV Bill of Sale form becomes invaluable for ensuring a smooth transfer of ownership.

Dd 214 - It details any reserve obligations after active duty service.