Download Mortgage Statement Template

Download Mortgage Statement Template

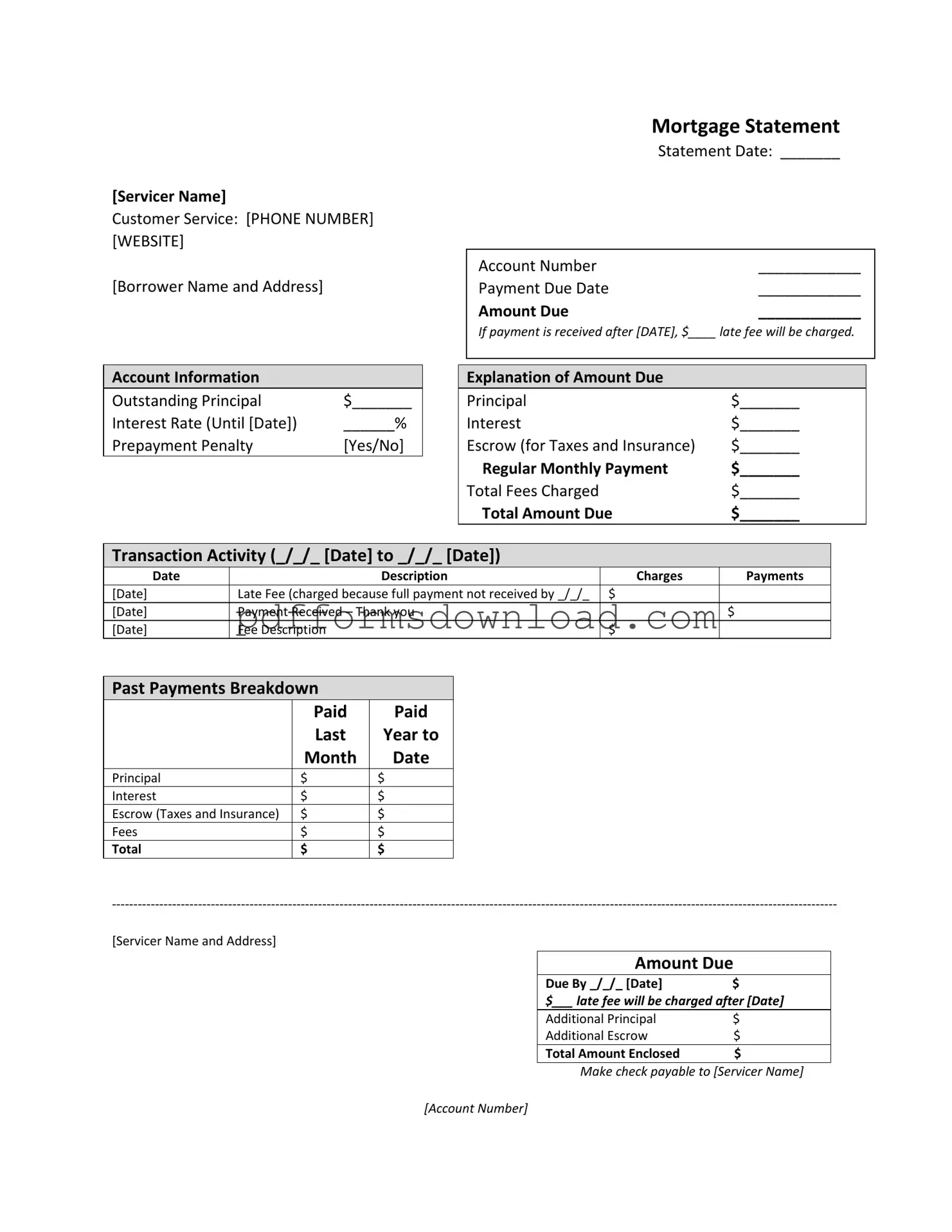

Incomplete Information: One common mistake is failing to fill out all required fields. Ensure that you provide your name, address, account number, and the statement date. Missing any of these details can lead to processing delays.

Incorrect Payment Amount: Double-check the amount due. Many people miscalculate their total payments or overlook additional fees. This can result in late payments or additional charges.

Ignoring Due Dates: Pay close attention to the payment due date. Late fees can accumulate quickly if payments are not made on time. Mark this date on your calendar to avoid penalties.

Missing Contact Information: Always include your servicer's contact information. If you have questions or issues, you need to know how to reach customer service. Failing to do this can lead to confusion later on.

Neglecting to Review Account History: Review your recent account history carefully. Look for any discrepancies or errors in payments. Addressing these issues promptly can prevent larger problems down the line.

When filling out and using the Mortgage Statement form, keep these key points in mind:

What is a Mortgage Statement and why is it important?

A Mortgage Statement is a document provided by your mortgage servicer that outlines your loan details. It includes important information such as the outstanding principal, interest rate, payment due date, and the total amount due. This statement is crucial for keeping track of your mortgage payments, understanding any fees, and ensuring you stay current on your loan. Regularly reviewing your Mortgage Statement helps you manage your finances effectively and avoid potential penalties.

What happens if I make a partial payment?

If you make a partial payment, it will not be applied to your mortgage balance immediately. Instead, the funds will be held in a separate suspense account. This means that your mortgage remains unpaid until the total amount due is received. To have the funds applied to your mortgage, you must pay the remaining balance of the partial payment. It's important to be aware of this, as it can affect your account status and may lead to late fees if the full payment isn't made on time.

What are the consequences of missing a payment?

Missing a mortgage payment can lead to serious consequences. If you fail to make a payment by the due date, you may incur a late fee. Continued delinquency can result in additional fees and potentially lead to foreclosure, which is the loss of your home. It's essential to address any missed payments promptly to avoid these negative outcomes. If you're facing financial difficulties, consider reaching out for mortgage counseling or assistance as soon as possible.

How can I contact my mortgage servicer for questions?

You can reach your mortgage servicer by calling their customer service number listed on your Mortgage Statement. They can provide assistance with any questions regarding your account, payment options, or other concerns. Additionally, many servicers have websites where you can find resources and information about your mortgage. Make sure to have your account number handy when you call, as this will help them assist you more efficiently.

When managing a mortgage, several forms and documents may accompany the Mortgage Statement. Each of these documents plays a vital role in ensuring that both the borrower and the lender have a clear understanding of the mortgage terms, payments, and obligations. Below is a list of commonly used documents that can help facilitate communication and clarify important details regarding your mortgage.

Understanding these documents can empower borrowers to make informed decisions about their mortgage. By staying organized and aware of each form’s purpose, individuals can navigate their mortgage journey with greater confidence and clarity.

I589 Form - The form can be completed by individuals without an attorney, but legal advice is often recommended.

The Ohio IT AR form serves as a crucial tool for taxpayers aiming to reclaim individual or school district income taxes, particularly after filing essential Ohio income tax returns like the Ohio IT 1040 or SD 100. By utilizing this application, individuals can accurately calculate their potential refunds, considering various payments and credits tied to their tax filings. For additional resources regarding this form, taxpayers can refer to Ohio PDF Forms to ensure they have the most up-to-date information and guidance.

Accident Report Form Template - This form can help facilitate any needed medical care.

Hiv Positive Report Pdf - Provides clarity on the performance of tests and operational procedures.