Printable New York Promissory Note Form

Printable New York Promissory Note Form

Inaccurate Borrower Information: Failing to provide complete and accurate details about the borrower can lead to confusion. Ensure that the full legal name, address, and contact information are included.

Missing Lender Information: Similar to borrower details, neglecting to fill in the lender's information can cause issues. Include the lender's name, address, and contact information.

Unclear Loan Amount: Writing the loan amount incorrectly can lead to disputes. Clearly state the amount in both numbers and words to avoid misunderstandings.

Omitting Interest Rate: Not specifying the interest rate can create ambiguity. If applicable, include the rate and whether it is fixed or variable.

Incorrect Payment Terms: Failing to outline payment terms, such as due dates and payment frequency, can lead to missed payments. Clearly define how and when payments should be made.

Neglecting Signatures: A common mistake is forgetting to sign the document. Both the borrower and lender must sign the note for it to be legally binding.

Not Dating the Document: Omitting the date can create complications in the enforcement of the note. Always include the date of signing.

Ignoring State Laws: Different states have specific requirements for promissory notes. Not adhering to New York's regulations may invalidate the note.

Failure to Include Default Terms: Not specifying what happens in the event of a default can lead to legal complications. Clearly outline the consequences of non-payment.

Not Keeping Copies: Failing to retain copies of the signed note can lead to disputes. Both parties should keep a copy for their records.

Filling out and using the New York Promissory Note form requires attention to detail and understanding of its components. Below are key takeaways to consider:

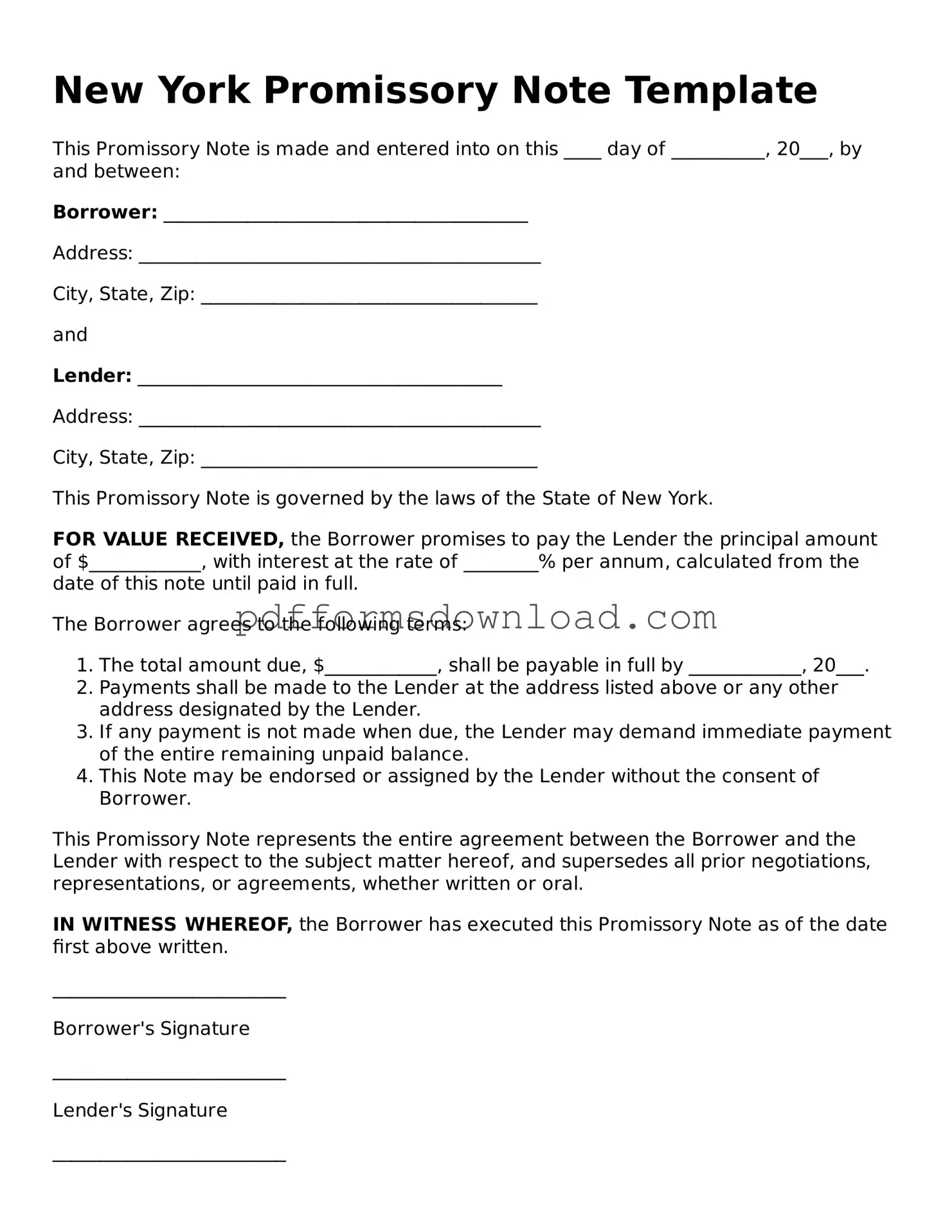

What is a New York Promissory Note?

A New York Promissory Note is a written agreement where one party promises to pay a specific amount of money to another party. It outlines the terms of the loan, including the repayment schedule, interest rate, and any penalties for late payments. This document serves as a legal record of the debt and the obligations of both parties involved.

Who needs a Promissory Note?

Anyone who is lending or borrowing money can benefit from a Promissory Note. This includes individuals, businesses, and organizations. It is especially important when the loan amount is significant or when the repayment terms are complex. Having a written note helps protect both parties by clearly stating the expectations and responsibilities.

What should be included in a New York Promissory Note?

A New York Promissory Note should include the following key elements: the names and addresses of both the borrower and the lender, the principal amount of the loan, the interest rate, the repayment schedule, any late fees or penalties, and the date when the note is signed. It may also include provisions for default and what happens in that case.

Is a Promissory Note legally binding?

Yes, a Promissory Note is legally binding in New York as long as it meets certain requirements. Both parties must agree to the terms, and the document must be signed. If either party fails to fulfill their obligations, the other party can take legal action to enforce the terms of the note.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the updated agreement. This ensures that everyone is on the same page regarding the new terms.

How do I enforce a Promissory Note?

If the borrower does not repay the loan as agreed, the lender can take steps to enforce the Promissory Note. This may involve sending a demand letter for payment or pursuing legal action in court. It is recommended to consult with a legal professional for guidance on the best course of action.

Do I need a lawyer to create a Promissory Note?

While it is not legally required to have a lawyer draft a Promissory Note, it can be helpful, especially for complex agreements. Many templates are available online, but having a legal professional review the document can ensure that it meets all legal requirements and adequately protects your interests.

When dealing with a New York Promissory Note, several other forms and documents may be necessary to ensure clarity and legal compliance. Each of these documents serves a specific purpose in the lending process. Here’s a brief overview of some commonly used forms:

Understanding these documents is crucial for both borrowers and lenders. Each plays a vital role in protecting interests and ensuring a smooth transaction. Be sure to review each form carefully to avoid potential misunderstandings in the future.

Promissory Note Virginia - It’s important for borrowers to understand their repayment obligations before signing.

For those in need of a legal resource, the available guide on the essential Quitclaim Deed template can simplify the process of property transfer. This document serves to clarify ownership without promises, making it particularly useful for familial arrangements or correcting title discrepancies. For further details, visit the essential Quitclaim Deed template.

Loan Agreement Template Texas - States the maturity date when the full payment is due.

California Promissory Note - This form is not just a promise to pay; it represents a critical part of financial responsibility and planning.