Official Owner Financing Contract Document

Official Owner Financing Contract Document

Failing to Clearly Identify the Parties: One common mistake is not clearly stating the names and contact information of both the buyer and the seller. This can lead to confusion later on.

Not Specifying the Purchase Price: The contract should explicitly state the total purchase price. Omitting this detail can create disputes down the line.

Ignoring Payment Terms: It is crucial to outline the payment terms, including the amount of the down payment, monthly payments, and the interest rate. Failing to do so can lead to misunderstandings.

Leaving Out the Loan Duration: The length of the financing period must be included. Without this, both parties may have different expectations regarding the timeline.

Not Including Default Terms: The contract should address what happens if either party defaults on the agreement. This can protect both the buyer and the seller.

Overlooking Property Description: A detailed description of the property being sold is essential. This should include the address and any relevant legal descriptions.

Neglecting to Include Closing Costs: Buyers and sellers often forget to specify who will be responsible for closing costs. This should be clearly stated to avoid any surprises.

Not Seeking Legal Advice: Many individuals attempt to fill out the form without consulting a legal expert. This can lead to significant errors that could have been avoided.

Failing to Sign and Date the Contract: A contract is not valid without signatures and dates from both parties. Forgetting this step can render the agreement unenforceable.

Using Inconsistent Language: Inconsistencies in terms and phrases can create ambiguity. It is important to use clear and consistent language throughout the document.

When navigating the process of owner financing, it's essential to understand the intricacies of the Owner Financing Contract form. Here are some key takeaways to keep in mind:

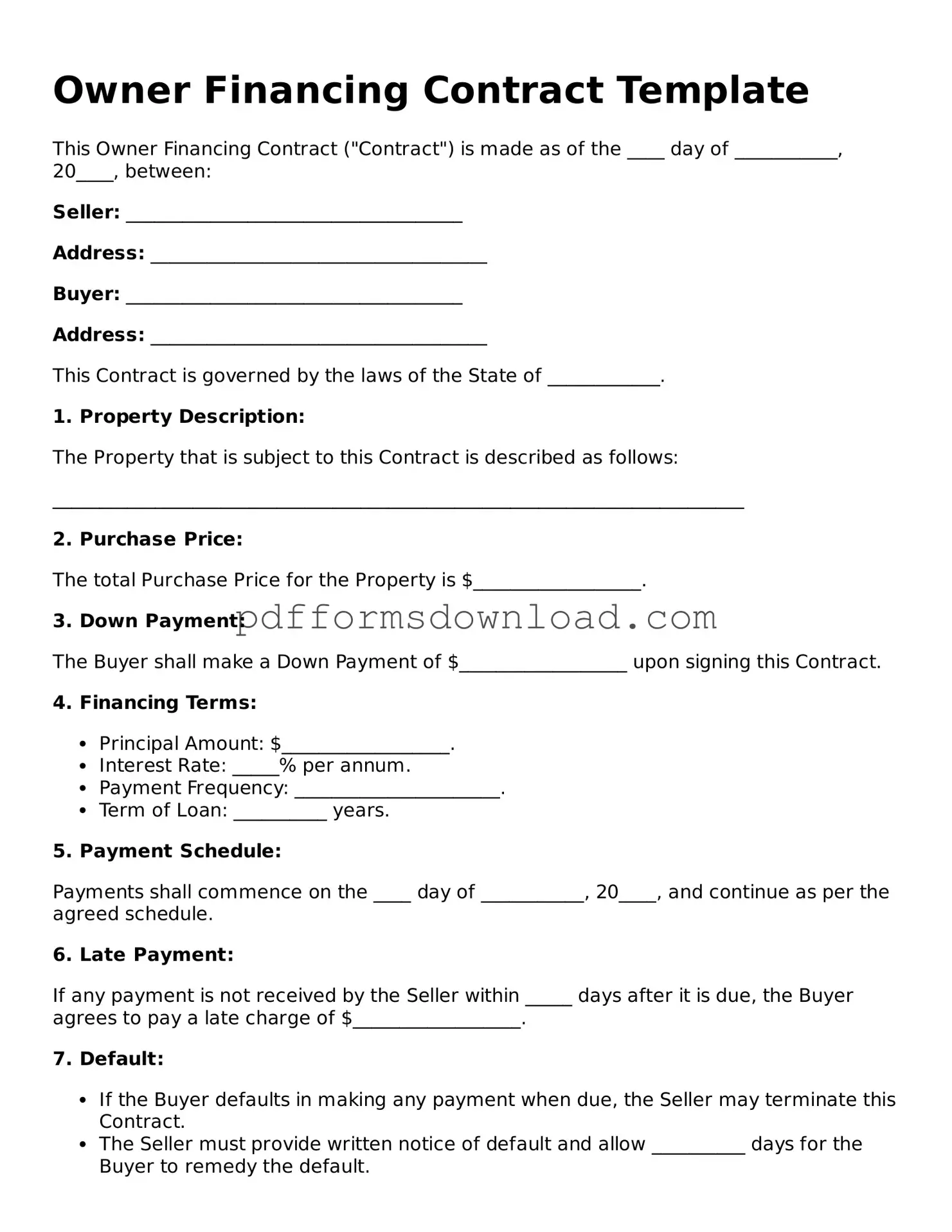

What is an Owner Financing Contract?

An Owner Financing Contract is an agreement between a seller and a buyer where the seller provides financing to the buyer to purchase the property. Instead of the buyer obtaining a traditional mortgage from a bank, the seller allows the buyer to make payments directly to them over time. This can make purchasing a home more accessible for buyers who may have difficulty securing conventional financing.

What are the benefits of using an Owner Financing Contract?

One of the main benefits is flexibility. Sellers can negotiate terms that suit both parties, such as the interest rate, down payment, and repayment schedule. For buyers, it can provide an opportunity to purchase a home without going through a bank. Additionally, sellers may find it easier to sell their property, especially if it has been on the market for a long time.

Are there risks associated with Owner Financing?

Yes, there are risks for both parties. Sellers may face the risk of the buyer defaulting on payments, which could lead to the need for foreclosure. Buyers might encounter issues if the seller has existing liens on the property or if the seller does not hold clear title. It is crucial for both parties to conduct due diligence and possibly seek legal advice before entering into such an agreement.

How is the interest rate determined in an Owner Financing Contract?

The interest rate can be negotiated between the buyer and seller. It often reflects current market rates but can vary based on the seller's willingness to finance the property and the buyer's creditworthiness. Both parties should discuss and agree on a fair rate that meets their needs.

What should be included in an Owner Financing Contract?

An Owner Financing Contract should include key details such as the purchase price, down payment amount, interest rate, repayment schedule, and any penalties for late payments. It should also outline what happens in the event of default and the process for transferring the title once the property is paid off.

Can an Owner Financing Contract be modified after it is signed?

Yes, an Owner Financing Contract can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the updated agreement to avoid future disputes.

What happens if the buyer defaults on the payments?

If the buyer defaults, the seller may have the right to initiate foreclosure proceedings, depending on the terms of the contract. The specific process and rights will be outlined in the agreement. It is important for both parties to understand these terms before signing the contract.

Is a down payment required in an Owner Financing Contract?

Typically, a down payment is required, but the amount can be negotiated. The down payment serves as a show of good faith and reduces the seller's risk. The specific terms regarding the down payment should be clearly outlined in the contract.

Can a buyer sell the property before the contract is fully paid off?

Generally, a buyer can sell the property, but they must first check the terms of the Owner Financing Contract. Some contracts may include clauses that require the seller's consent before the property can be sold. It is essential to review the contract carefully and consult with a legal professional if needed.

Should I consult a lawyer before signing an Owner Financing Contract?

Yes, it is advisable to consult a lawyer before signing an Owner Financing Contract. A legal professional can help ensure that the contract is fair, complies with local laws, and protects your interests. This step can help prevent potential issues down the line.

When engaging in an owner financing arrangement, several other forms and documents may be necessary to ensure a clear and legally binding agreement. These documents help outline the terms of the financing, protect the interests of both parties, and provide necessary disclosures. Below is a list of commonly used documents that accompany the Owner Financing Contract form.

Utilizing these documents in conjunction with the Owner Financing Contract form can facilitate a smoother transaction. It is essential for both buyers and sellers to understand each document's purpose to ensure a successful owner financing arrangement.

Purchase Agreement Addendum - Addresses any negotiations made regarding inspections or assessments.

In addition to understanding the significance of the Texas Real Estate Purchase Agreement form, it is essential to have access to reliable resources that can guide you through the process. For comprehensive information and templates, you can refer to Formaid Org, which provides valuable insights for both buyers and sellers in Texas real estate transactions.