Official Promissory Note Document

Official Promissory Note Document

Incorrect Borrower Information: One common mistake is failing to provide accurate information about the borrower. This includes the full legal name, current address, and contact details. Any discrepancies may lead to complications in the future.

Missing Loan Amount: It is essential to clearly state the amount being borrowed. Omitting this information can create confusion and disputes later on.

Failure to Specify Interest Rate: Not including the interest rate or leaving it blank can lead to misunderstandings regarding the cost of the loan. Clearly defining the rate helps both parties understand their obligations.

Omitting Repayment Terms: Repayment terms should be detailed in the note. This includes the payment schedule, due dates, and any grace periods. Vague terms can result in disagreements down the line.

Not Including Signatures: A promissory note must be signed by both the borrower and the lender. Failing to do so renders the document unenforceable. Ensure all parties involved have signed the note.

Neglecting to Date the Document: Not dating the promissory note can lead to issues regarding the timeline of the loan. A date provides clarity on when the agreement was made and can be crucial in legal matters.

When filling out and using the Promissory Note form, there are several important points to keep in mind:

What is a Promissory Note?

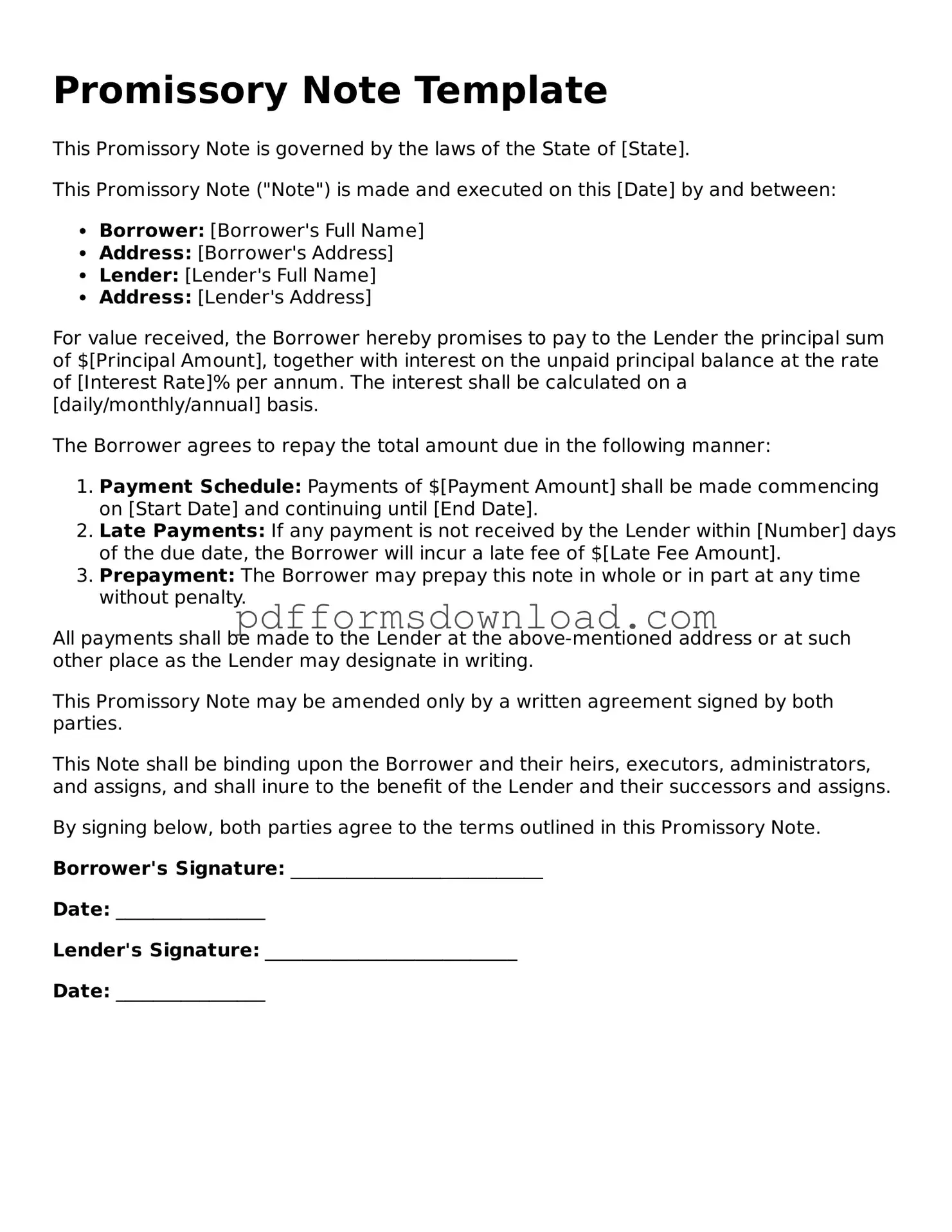

A Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. It outlines the terms of the loan, including the principal amount, interest rate, and payment schedule. This document serves as a legal record of the agreement between the borrower and the lender.

Who uses a Promissory Note?

Individuals and businesses commonly use Promissory Notes. They are often utilized in personal loans, business loans, and real estate transactions. Anyone who lends money or extends credit may require a Promissory Note to formalize the arrangement and protect their interests.

What are the key components of a Promissory Note?

A typical Promissory Note includes the following key components: the names of the borrower and lender, the principal amount, the interest rate, the repayment schedule, and any late fees or penalties. It may also specify whether the loan is secured or unsecured and include provisions for default.

Is a Promissory Note legally binding?

Yes, a properly executed Promissory Note is legally binding. Once signed by both parties, it creates an enforceable obligation for the borrower to repay the loan according to the agreed-upon terms. If the borrower fails to repay, the lender can take legal action to recover the owed amount.

Do I need a lawyer to create a Promissory Note?

While it is not mandatory to hire a lawyer, consulting one can be beneficial. A lawyer can ensure that the Promissory Note meets all legal requirements and adequately protects your interests. However, many templates are available online for those who prefer to draft their own notes.

Can I modify a Promissory Note after it has been signed?

Yes, you can modify a Promissory Note, but both parties must agree to the changes. It is best to create a written amendment that outlines the specific modifications. This document should be signed by both the borrower and the lender to maintain its enforceability.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has several options. They may choose to negotiate a new payment plan, pursue legal action to recover the owed amount, or initiate foreclosure if the loan is secured by collateral. The specific actions taken will depend on the terms outlined in the Promissory Note and applicable state laws.

A Promissory Note is a crucial document that outlines a borrower's promise to repay a loan to a lender under specified terms. However, several other forms and documents often accompany a Promissory Note to ensure clarity, security, and legal compliance in the lending process. Below is a list of related documents that are commonly used alongside a Promissory Note.

Using these documents in conjunction with a Promissory Note can help ensure that both parties understand their rights and obligations. Proper documentation not only protects the lender's interests but also provides the borrower with a clear understanding of their responsibilities.

General Affidavit Template - Affidavits can also affirm compliance with laws or regulations.

What Information Must Be Listed on a Job Application? - Completing this form is the first step toward your new job.

For individuals navigating the legal system in California, completing the California Affidavit of Service form correctly is essential. This document not only serves as proof of delivery but also ensures that all parties are properly informed about the legal proceedings. To assist with this process, you can visit californiadocsonline.com/affidavit-of-service-form for guidance on the requirements and submission procedures, helping to uphold the integrity of the legal process.

I589 Form - The I-589 must be submitted in a timely manner to preserve eligibility for asylum based on timely filing requirements.